Buying a home can be stressful. Assets like property can appreciate - but when you buy can mean paying more now, or later. It can be confusing when you are trying to balance how much down payment you have (or need) with the rise and fall of interest rates.

One thing is for sure, waiting on buying a home in today's economy could be costing you big money. We are going to explore 11 ways you may be losing money by not letting Navy To Navy Homes help you in the process of buying a home now.

By renting a home you are losing money that you could be putting toward an investment.

Renting a home can make sense when you are not sure where you want to live, if you are in the military, or if you are prone to moving for work. Something to keep in mind is that every dollar you put toward rent is a dollar you will never get back.

Many economists suggest buying a home as young and as soon as you can - for the best potential investment. Even a small starter home in a not-so-great - neighborhood is still an investment you can cash in on later.

By making a conservative home purchase early in your life could set yourself up to purchase your dream home later.

Rent can go up at the whim of your landlord.

In a lot of the United States right now the rental market is booming!! According to ApartmentTherapy.com, “typically rent increases with inflation at about 3% per year”, but that can be much higher in hot markets.

This does not mean that your rent will go up each year at renewal. Some places do an across the board rental increase every two or three years depending on upgrades made to the property and market trends in the area.

There are cities, and now even states, having to mandate rent control to keep landlords from price gouging their tenants. Some landlords refuse to extend a lease because they know they can hike the rent by several hundred dollars for the next tenant.

As of 2018, there were only 4 states with Rent Control laws on the books. Oregon was added to that list in March of 2019 and now Illinois is looking at similar legislation.

_1.png)

Tax savings can really add up.

Another thing that will save you money as a homeowner vs. a renter is the tax savings of having a mortgage.

One tax benefit of buying a home is the mortgage interest deduction. Homeowners can deduct the interest they pay on a mortgage for costs related to buying, constructing, or improving their home.

According to LendingTree, “home buying also promises more immediate tax benefits, like deductions on mortgage interest or property tax payments that might help shave a year-end tax bill.”

Your home is an asset that could be borrowed upon in an emergency.

Depending on when you purchase your home and how much equity you amass, you could borrow against the value of your home in an emergency.

How much equity do you have? It is simple math. If you take the $200,000 value your home is appraised at and you still owe $150,000, your available equity is $50,000. That is 50K you can “borrow” against your home.

This new loan is often referred to as a second mortgage. If you sell the home you must first pay off the second mortgage.

According to Discover.com, “A home equity loan can be a good option if you need to cover large expenses associated with home renovations, college tuition, consolidating debt, or other types of major expenses. Because you can borrow against the value of your home, a home equity loan may also be easier to qualify for than other loans because the loan is secured by your house.”

The loan money you might not qualify for otherwise could be right there in your home. If credit card debt or medical bills have added up over time you could bail yourself out by borrowing against the equity in your home and get things consolidated to a lower interest rate.

Interest rates could go through the roof at any time.

Mortgage interest rates are known to fluctuate, sometimes daily. If interest rates are high, borrowing money for your home will cost more. If the interest rates are low, your mortgage payment will be smaller and you'll pay less in interest over the life of your loan.

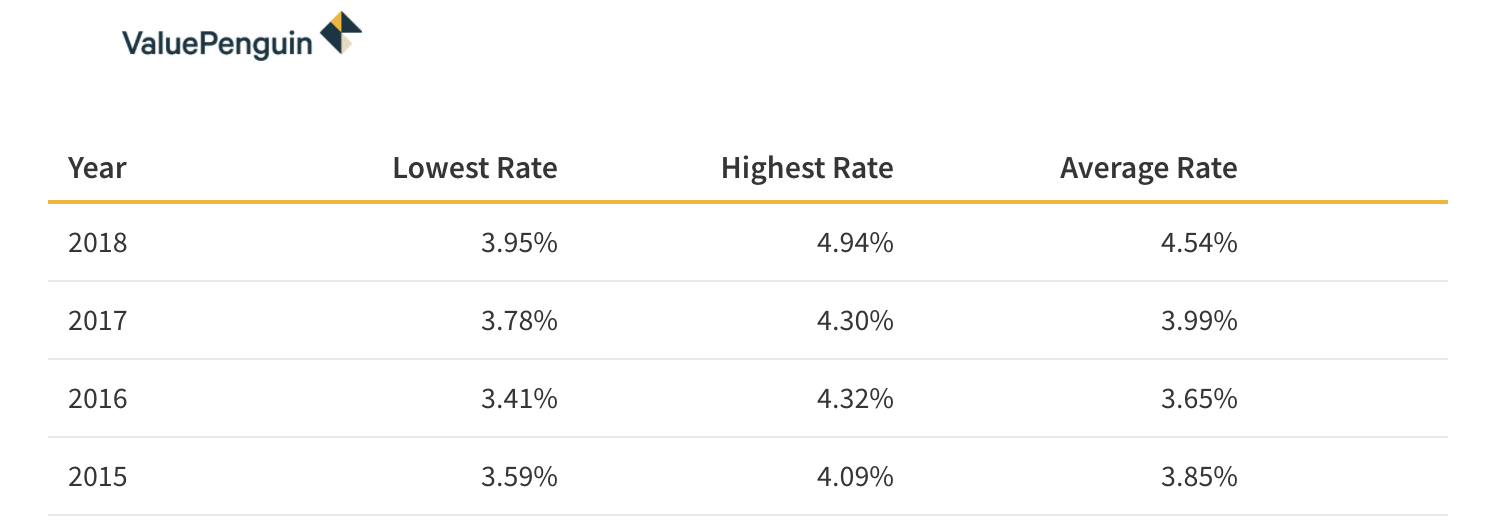

As you can see in the image below interest rates are higher now than they were in years past. After the housing bubble burst in 2008 we saw the lowest interest rates ever. Now that interest rates have had time to normalize we could be looking at some steady increases for the coming years.

We all know that your credit score matters, but it is not everything. Interest rates can change and you could have no control if you are not locked into a lower rate.

Looking at the image below you can compare just the difference between the lowest 2018 interest rate of 3.95% to the average interest rate of 4.54%. The small difference of only .59% could save you almost $25,000 in interest over the life of your loan.

Historical average Mortgage Interest Rates have ranged from as high as 18.63% in 1981 to as low as 3.31% in 2012 after the bubble burst.

.png)

There is good news about those rising rates. If in several years you have paid consistently and improved your credit score and debt to income ratio you could always refinance if the interest rates start to fall.

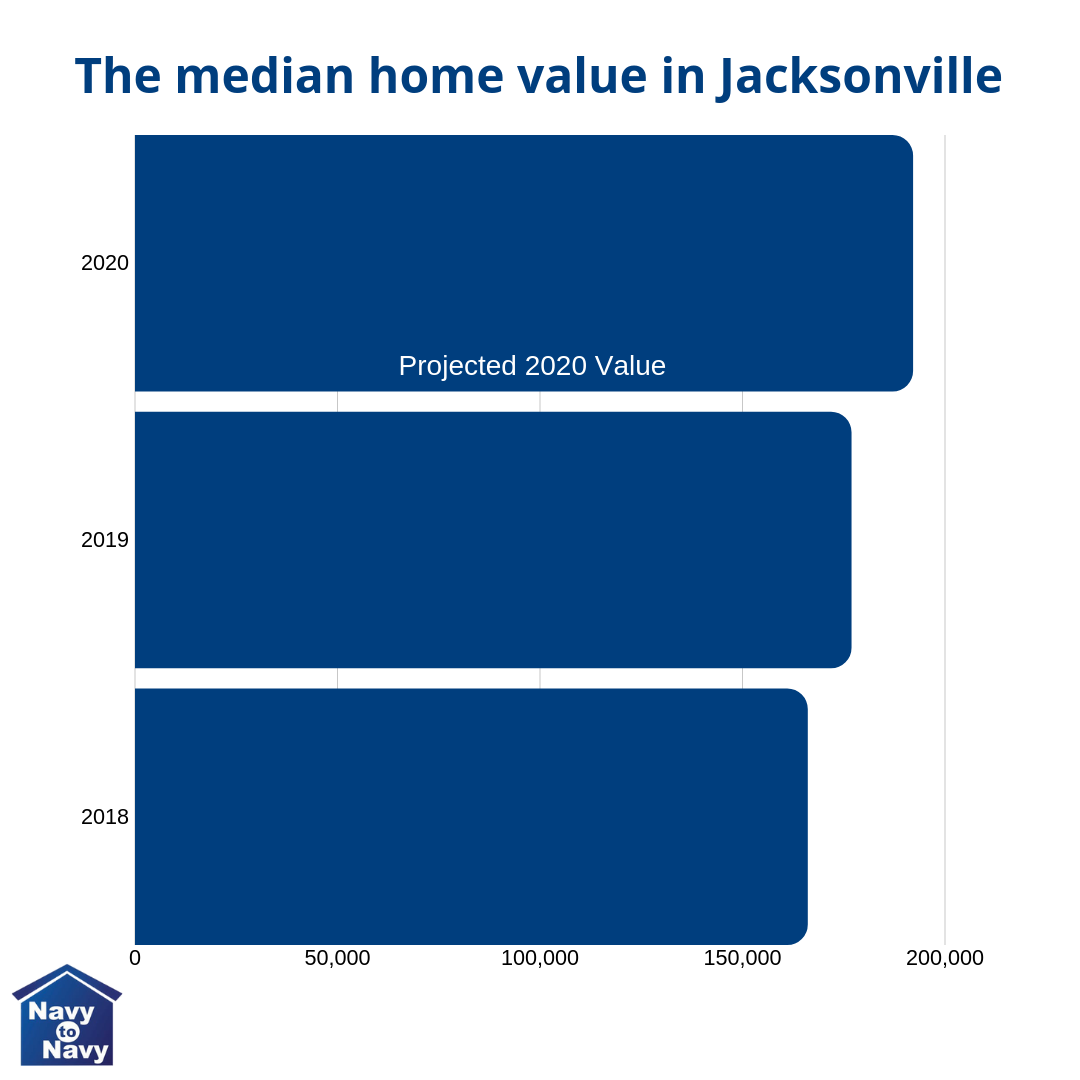

In Jacksonville right now the average home price went up a startling 6.8% last year. Even at half that, the projected increase of 3.6% in the coming year is still a good chunk of money.

“The median home value in Jacksonville is $176,800. Jacksonville home values have gone up 6.8% over the past year and Zillow predicts they will rise 3.6% within the next year.”

Will your interest rate go up by one or even two percent? Could a situation arise that will cause your credit score to drop? Could you change jobs and increase your debt to income ratio or limit the money you thought you could save over that time period?

Freddie Mac predicts interest rates to rise to 5.1% by the end of 2019.

CoreLogic predicts home prices to appreciate by 4.8% over the next 12 months.

Waiting could mean paying more for the same house in just a few months time.

Whether it is higher pricing because of inflation or just because certain times of the year command higher prices, waiting to buy a home could cost you money.

Waiting only a few months to purchase could cost you $5000-$7000 on the average home for sale in Jacksonville. Will saving for a bigger down payment over 3-6 months really save you in the long run? Only if you can save more money than the increased value of the homes you are looking at.

Another issue is that you could miss out on the perfect house for you. Finding the right home is not always easy. There are many factors to consider such as location, amenities, style, etc.

If you hold off on home buying there is no way of know if that house in that perfect neighborhood will still be on the market. You may have to settle for something less than ideal if you wait. Especially if the prices jump up further than currently expected.

Making others rich is never a better idea than creating an asset for yourself.

I get it, buying a home is a huge investment and can be a stressful decision. That should not hold you back from making an investment in your own future. You can continue to rent indefinitely and keep filling the pockets of those your rent from or you can invest in your own future.

If you decide a few years down the road to move you can choose to cash out your investment and buy elsewhere or rent out your home to someone else. Having rental property in a hot market can also add to your investments.

You could use your house as a savings plan to pay for something else in the future.

If you have a child going to college or find a great vacation cabin you might be able to borrow against your home's value to fund those dreams. Maybe it is finally buying a boat because you bought near the water all those years ago.

Buying now as the market is on the upswing may allow you to get that swimming pool you have always wanted. By purchasing sooner within your budget you could plan for future improvements as you have the equity in the home to support them later.

Or consider fixer upper homes, where you can double your profit! If you can live in it 2 years+ while you work on it, you don't have to pay Capital Gains tax.

Invisible costs and deadlines...

Not all housing decisions have an obvious financial consequence. Some reasons for buying will cost you time not just money.

Are you looking at homes in a particular area based on the commute? How about where your children go to school or where you WANT them to go to school?

For some, the commute between work and home is a costly factor. If you have changed jobs and increased your distance between work and home it might be time to just buy in the neighborhood that will decrease the time and distance.

You could save hundreds or even thousands by reducing your fuel and wear and tear costs on your vehicles. Never mind the time you could get back with your family if you lived closer to work. What is that time worth to you?

By waiting to buy you could find yourself stuck in another year lease on your rental because you do not want to move the kids mid-school year. If you find a home before you are locked into another year of rent you could start increasing equity in your own home

Picking the wrong time of year could cost you.

An often overlooked factor in the price of a home is what time of the year you purchase. Buying a home at the wrong time of year could cost you big.

Supply and demand are always a factor in the home buying process. During certain times of the year, supply can dip creating a Seller Market.

Many people wait until Summer to move. Waiting for kids to finish a school year or just waiting for better weather to pack up in can be factored into a move. Summer tends to have more homes on the market because of those things.

There are more homes on the market than buyers that are also looking to move during this time. Again, people are concerned with making the move when the weather is nice and the kids are between school years.

Waiting until winter when demand wanes might save you when buying a home. Waiting for demand to dip could save you thousands.

Your new home could be your future rental property.

Even if you are unsure of what your future holds, buying a house now could become a future income property.

Buying a home now does not commit you to living in it forever. You will have the option to sell or even rent out that home in the future.

Having a rental property could make you money for years to come if your situation changes. Then have the option to be a landlord or hire someone like Navy To Navy Homes to manage your property for you.

So, what are you waiting for?

If you are done waiting to buy a home then the wonderful professionals at Navy To Navy Homes are waiting to help. They can help you navigate the ins and outs of mortgages, credit scores, help you find the right neighborhood, and take care of all of the details to get you into your new home.

Mario and his caring team of brokers and realtors at Navy To Navy Homes will take care of all of the details making your home buying purchase as easy as possible.

Navy to Navy Homes

4540 Southside Blvd, Suite 702

Jacksonville, FL 32216

904-900-4766