Do You Have a Plan for Sending Your Child to College?

As a parent, it is important not only to have high hopes for your child’s future, but also to actively build a plan to make those dreams come true.

Planning at this scale might seem overwhelming, but it doesn’t have to be.

Getting into real estate is a terrific way for you to start saving for your child’s college education, and it isn’t complicated.

Step 1 - Estimate College Costs

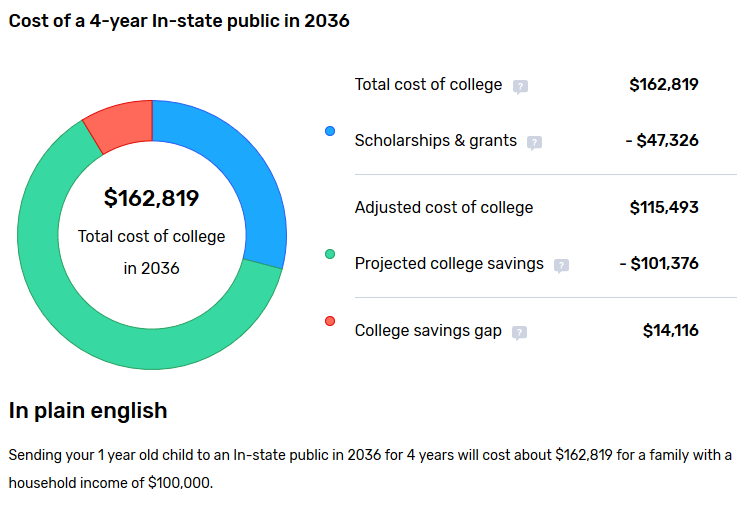

The first step is to get an idea of how much it will cost to send your child to college. Use this handy college savings website to calculate an estimate. All you have to do is plug in some numbers and you will have a forecast of what college will cost by the time your child is ready to attend.

As you can see, for a household with an annual income of $100,000, it would cost $162,819 to send one child to college in 2036. From there, your investment will vary depending on several factors.

Factors to consider:

Will your child go to a public or private school?

Will he or she go just 4 years or is graduate school in the plan?

Will you fund 100% or will your child contribute a personal investment?

Regardless of how much you plan to contribute to your child’s college tuition costs, college is a major investment that can be a big source of stress to parents, who are wondering how they are going to afford it. Wouldn’t it be great to find a way to make that money easily?

The numbers can feel a little intimidating at first, but once you know what you need to plan for, you can set your child and your family up for financial success. A sound plan can ensure that your child is able to attend college and act as a safeguard against incurring massive student loan debt that will follow him or her well into adulthood.

The pressure of student loan debt is a huge issue even today and will likely only get worse. There are plenty of professionals who wear the “golden handcuffs” and feel stuck in dead end jobs because they have student loan payments to make for the next 30 years. Let’s make a plan for your child to avoid the stress of graduating with exorbitant student loan debt, so he or she can start a career with a clean slate and minimal debt.

Make a plan as soon as you can. Don’t wish. Plan. And start now. It is never too early.

“It takes as much energy to wish as it does to plan.” – Eleanor Roosevelt

Planning doesn’t have to be complicated, and there’s no reason your child can’t go to a good school.

With a little planning, you can give your child the future he or she deserves.

An accurate and realistic forecast and budget are critical, because you really only have about 10-18 years to get ready for your child’s education expenses. You can do this and we can help.

Step 2 - Determine Your Savings Strategy AKA Your “Portfolio Market Mix”

Get Started With The Right Savings Plans and Accounts

1) 529 plans

Legally known as a “qualified tuition plan,” a 529 plan is a specialized savings plan that allows you to save money specifically for your child’s education and the expenses associated with it.

Pros:

Contribute high amounts - up to $300,000 in some states

No income limits

Investment growth is tax-free

Cons:

If your child decides not to go to college, the money is frozen

There could be high fees involved in accessing the money, if your child opts for trade school, military, or an entrepreneurial career

Transferring the funds to another child can be tricky

For other limitations, check out this article on 529 plan limitations from Bank of America Education Savings Program Director, Richard Polimeni.

2) Prepaid college tuition plans

These plans involve purchasing “units” from a college. This means that the tuition price you save for is locked in at the time of enrollment and you get to avoid inflated tuition costs.

Pros:

Lock in the price of tuition

Uninflated tuition cost

Transferable between children

No limit on contribution amounts, so you don’t need to make any investment decisions until you are ready

Cons:

Funds can only be used for tuition and fees, not for housing, supplies, and other related expenses

Limited control over how the funds are invested

Some plans are limited to in-state colleges only. If your child gets a scholarship for an out-of-state school, limitations apply.

For information on Florida State Prepaid college plans, check out Florida's College Savings Plans page.

*Be aware that there are downfalls to this option. According to NASDAQ, you can run the risk of your state becoming unable to back the funds. This happened to some families in Alabama, so make sure to investigate the rules in your state and plan well. (Florida's plan is guaranteed by the state of Florida - but be sure to ask questions when you call.)

Remember, if you go this route, plan to have another type of savings for the other expenses. Prepaid tuition plans cover tuition only. They don’t cover room and board, books, or any other expenses. Life happens while in school so you will need to plan for those extras.

3) Uniform Gifts to Minors Act (UGMA) and/or Uniform Transfers to Minors Act (UTMA):

This option is a type of custodial account that allows adults to transfer assets to minors.

These accounts are basically trusts that let a third party hold assets for a beneficiary. You, the grandparents, aunts and uncles, or whoever wants to can put money in this account for your child.

According to SmartAsset.com, “A UGMA account is limited to purely financial products such as cash, stocks, mutual funds, bonds, other securitized instruments and insurance policies.”

A UTMA account can hold any form of property, including physical property and real estate. For example, a parent could put his or her car or even the deed to a family home into an UTMA account.

Note that all states have adopted the UGMA whereas Vermont and South Carolina do not allow UTMA accounts.

Pros:

Tax advantages for the contributor

The investment decisions are made for you

The money is secure and protected from creditors, other family members, or any third parties

The beneficiary receives the money at the age he or she is designated to receive it

Cons:

A UGMA account is limited to purely financial products

Vermont and South Carolina do not support UTMA accounts

4) Coverdell education savings account:

This account is a tax-deferred trust that assists families with educational expenses. It is an after-tax account.

Pros:

Investment flexibility

Not state-run

You can use the broker of your choice

Not limited to a particular college

Cons:

Limited to $2,000 in contributions per year

Don’t qualify for state tax benefits

5) Real Estate

With real estate, you have a versatile investment form that you can use to power up any of the other options and shield yourself from their downsides.

Real estate allows you to have flexibility in how you spend the money you save. It lets you control more of the variables such as where you buy, who you rent to, etc.

Getting involved in real estate is a great way to help you make money for your child’s future. While there is some risk involved with owning rental properties, partnering with an experienced property management company or real estate professional like one of our team members at Navy to Navy here in Jacksonville, Florida can help you mitigate some of that risk and turn this option into a passive income stream.

A skilled realtor and property management company can bring in passive income for you while you simultaneously grow your child’s college savings fund with minimal effort. Nothing else will let you build your investment as aggressively as real estate.

This article reviews "How To Make Money While Using a Property Management Company".

In this Forbes article, one dad purchased a piece of property when his child was 6 months old. The tenants will make payments for the next 18 years. Then, when it is time to pay for college, he will sell or refinance the property. Since the property value will continue to increase, he will be able to fully fund his child’s college education.

The benefit of property management is that it offers flexibility. Parents can control the variable and then use the money as they want to fund their child’s education. The use of this money won’t be limited to only tuition or fees like some of the other plans, which means that it can be applied where it is most needed. That means this route lets parents provide for it all.

And the beauty is that property management doesn’t have to be complicated with the right help.

Get Ahead With Real Estate

There are many options (even more than what is outlined here!). Each strategy has its own set of advantages and disadvantages.

But there is a way to offset the cons of any of these them: by diversifying your strategy and adding real estate investing into the mix - particularly, acquiring a rental property.

How does this work?

A rental property in a great real estate market like Jacksonville, Florida can offset the saving burden by providing extra cash flow each month. Saving properly for your child’s future doesn’t have to eat into your available resources or limit what you can do and provide for them now.

But even if you’re not having a problem sticking to your savings schedule and budget, the right rental property could provide surplus income that you could also funnel into your child’s savings account so that you can reach your goals that much faster and without feeling any kind of pinch. Not much else will give you those kinds of returns. Isn’t your child’s future worth it?

With a rental property properly chosen and cared for, your renters pay your mortgage and build your equity while you spend your own hard-earned cash elsewhere.

Step 3 - Make The Phone Calls. Get Started.

All the dreaming and the planning in the world won’t help you save for your child’s college. You have to take action.

Reach out to a recommended financial advisor for help with stock market options (like 529 plans).

For physical growth assets, like real estate, talk to a trusted and well-reviewed real estate professional.

Diversify and Empower Your Future With Real Estate

Adding a real estate asset to your savings plan for your child not only diversifies your savings approach so your eggs aren’t all in one basket, restricting you or your child to a certain path or to a certain school, but it also supercharges any of these plans and allows you greater flexibility as well as the return on investment for your own future too.

And, to speak of the unspoken white elephant in the room, in the event of an emergency, or that your child decides not to go to college, you can always sell the property (with all your equity) and keep the profit or apply it to your child's wedding or business start-up expense. Other investment options will not allow you such flexibility and impose a fee or penalty for life changes like these.

To ensure you can reap all these benefits, be sure to receive a consultation and get professional help as you would with any investment. There is a learning curve at times.

Our team here at Navy to Navy in Jacksonville, Florida, has almost two decades of experience in real estate and is ready to help you make the perfect choice today.

Have questions about investing in real estate for your child’s future? We’d love to help.

Navy to Navy Homes

4540 Southside Blvd, Suite 702

Jacksonville, FL 32216

904-900-4766